Permissionless Kaia: Rewriting the Terms of Openness

Kaia Technical Roadmap Deep Dive Series: Part 1

Last week, the Kaia team unveiled the Kaia Technical Roadmap, outlining a vision to become the foundational infrastructure for onchain finance across three core pillars. At the forefront is Permissionless Kaia: a comprehensive overhaul of validator participation, governance, and tokenomics.

This article is the first deep dive in the series, and it walks through the Permissionless Kaia pillar in depth. But the point isn't simply to explain what Kaia is shipping. These questions go well beyond Kaia. As public chains become the infrastructure institutional capital actually moves onto, the entire industry is facing the same set of questions. Who gets to participate in the network and how? What should governance look like, and what accountability does it need to carry? How should rewards tie to the value a network actually creates? And ultimately: does the word "permissionless" we inherited from the early public-chain era still mean the same today?

We believe the answers are beginning to diverge in meaningful ways across the industry. This piece starts by framing that broader landscape, then explores why Kaia has taken its particular approach.

1. "Permissionless" Doesn't Mean What It Used To

In the early days of public chains, permissionless was a simple word. Anyone could participate in the network and run a node. Anyone could participate in governance forums. Anyone could run mining hardware or stake tokens to become a miner or validator. The word literally meant "anyone can participate," and its opposite was "permissioned."

In 2026, that binary no longer holds. As stablecoin payments move beyond crypto-native users — the so-called Degens — and into institutional settlement rails, and as tokenized assets, RWAs, and payment/remittance infrastructure start landing on public chains, the questions a network has to answer have become much more concrete.

What institutions look at when evaluating a public chain comes down to two perspectives. The first is predictability, meaning the confidence that problems won't occur. The second is clarity of accountability, because even with the best prevention, things could break, and someone has to own the fix. When either axis wobbles, no amount of TVL, low fees, or high TPS will make institutional capital willing to commit.

Those two axes translate into a practical checklist:

- How fast are transactions processed onchain, and under what conditions do they become irreversibly final?

- When something breaks, who is accountable, and how is it recovered?

- Are fees not just cheap, but stable, transparent, and invisible to the user?

- Who can change protocol parameters, and how traceable is the decision path?

- Do token incentives connect to network value, or are they just sell pressure?

Measured against that checklist, "anyone can run a node" may be a necessary condition, but it isn't a sufficient one. In fact, here's the paradox: the more capital and accountability a public chain carries, the more the network wants to restrict participation again. The fastest way to give institutions both predictability and accountability in one step is to limit validators to a known few.

Many recent designs across the industry are yielding to this temptation—each in their own way.

2. The Two Answers the Market Has Offered

2.1 Institution-friendly networks: buying predictability at the cost of curated participation

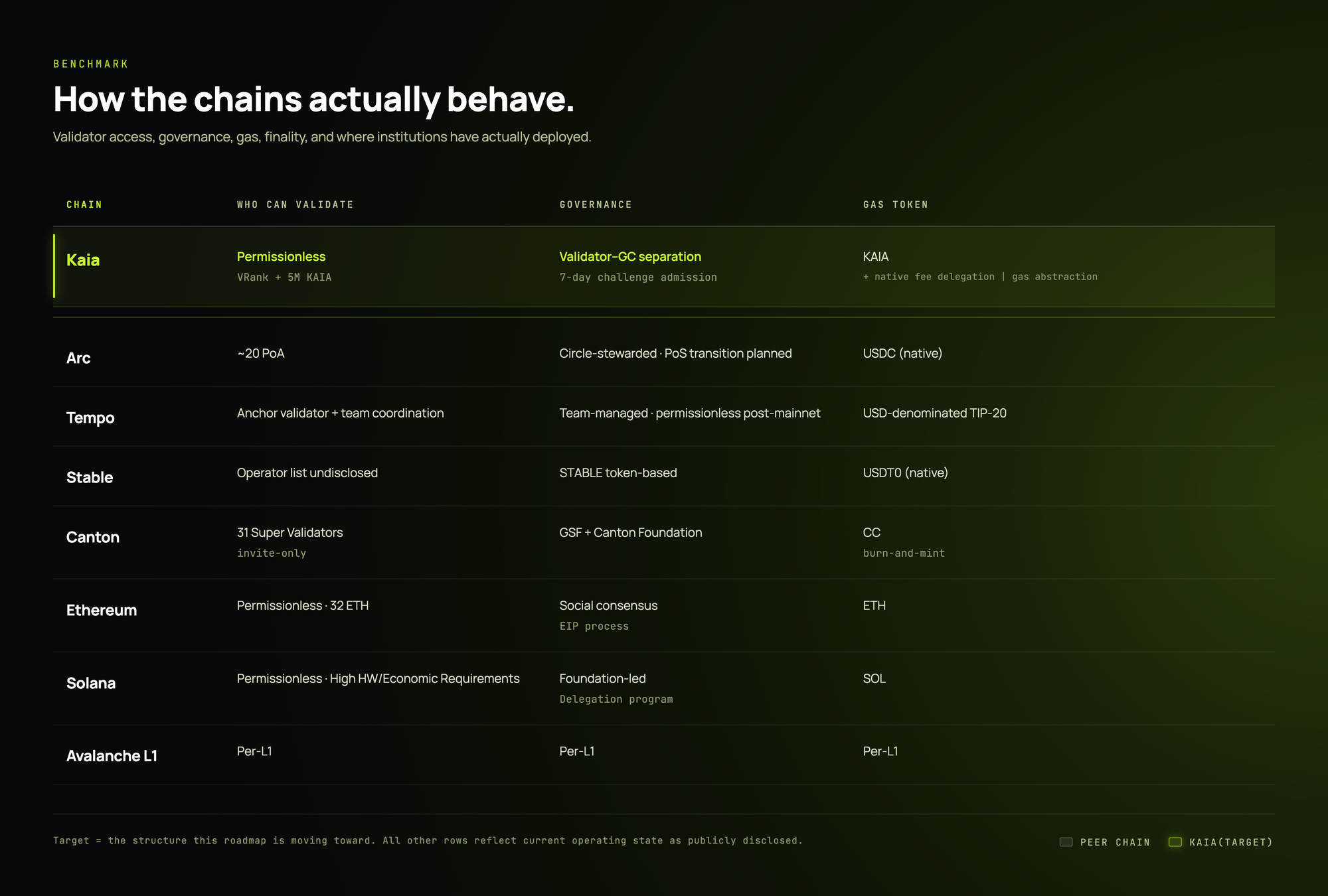

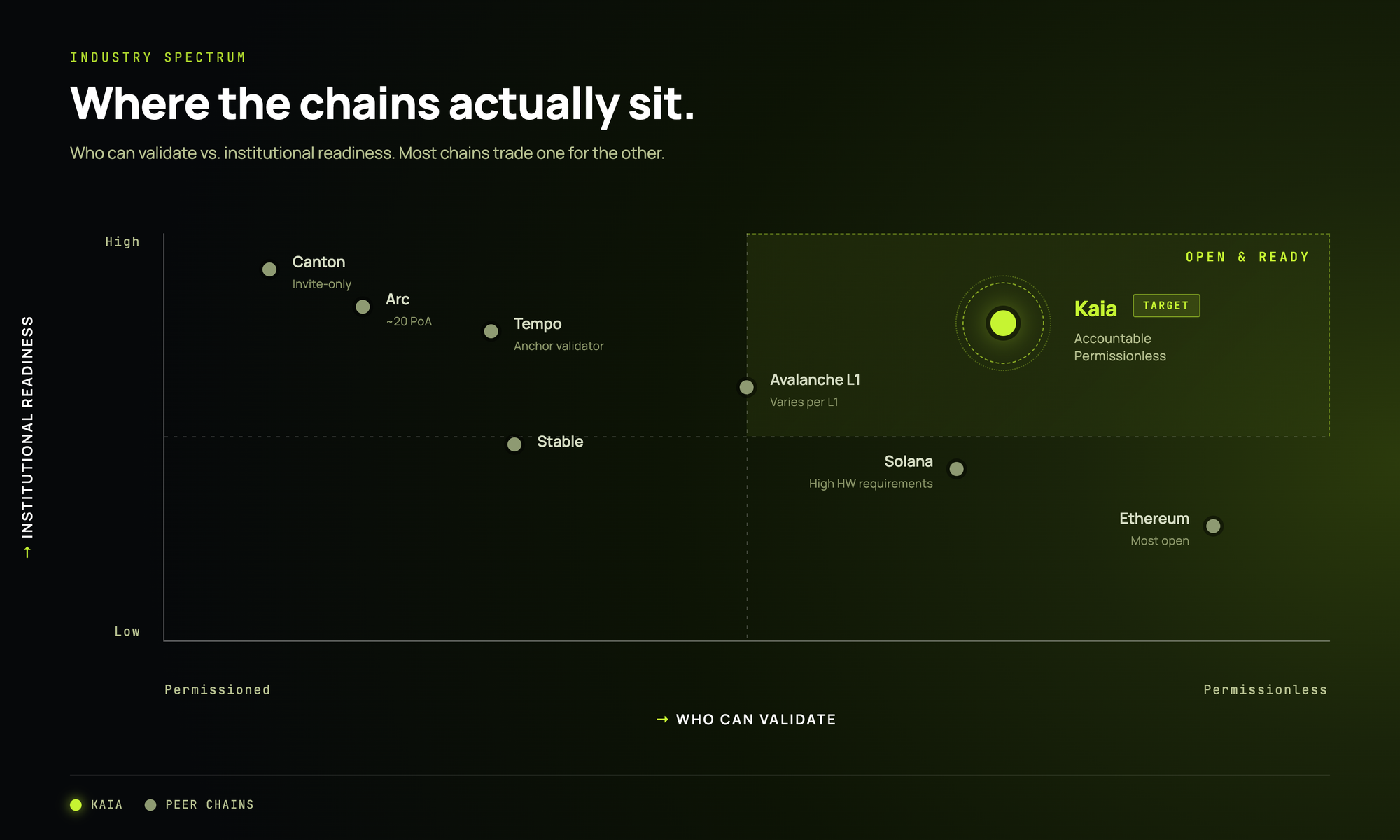

Circle’s Arc has focused on developing an institution-friendly approach. It uses USDC as the native gas token, targets dollar-denominated fees of around one cent, and leads with sub-second deterministic finality (built on Malachite BFT) and opt-in privacy. The consensus layer today is a Proof-of-Authority (PoA) model run by roughly 20 regulated institutional validators, all SOC 2 certified. The identities of those 20 validators, though, haven't been publicly disclosed. BlackRock, BNY, Goldman Sachs, Visa, Mastercard, AWS, Anthropic, and more than a hundred other institutions are listed as Arc testnet participants, but they're all classified as "ecosystem participants" rather than named validator operators. At a Seoul event in April 2026, Circle CEO Jeremy Allaire said the company is considering launching a native token for Arc and transitioning to Proof-of-Stake (PoS). The official roadmap spells out a move from "permissioned PoA to permissioned PoS." The starting point is institutional curation, but the long-term direction is phased decentralization.

Tempo, a payment-focused L1, takes a different angle. It has no native gas token. Fees are paid in USD-denominated TIP-20 stablecoins. Block time sits around 0.5 seconds, deterministic finality is the default, and payment-friendly features like fee sponsorship and batch calls are built directly into the protocol. A TIP-403 policy registry lets issuers apply compliance rules down to the gas-transfer level. In April 2026, Visa joined as an anchor validator, with Stripe and Zodia Custody (a Standard Chartered subsidiary) signing on as early external validators.

Note on "anchor validator": Tempo's official documentation doesn't define the term as a formal tier in the consensus layer. Based on the wording in Visa's press release, it's closer to a marketing label for external validators that help verify transactions early on and accelerate onchain payment infrastructure. In practice, the role is to have known payment and custody firms underwrite initial trust until the network matures. Tempo's public roadmap says it will go fully permissionless after mainnet, but validator onboarding today still requires "coordination with the Tempo team."

Stable, a chain tightly coupled itself to to the Tether ecosystem, has taken yet another path. After launching mainnet in December 2025, the v1.2.0 upgrade in February 2026 made USDT0 the native gas token. The previous wrap step is gone; users can transact with just USDT. Security and governance are handled by a separate STABLE token. With a total supply of 100 billion, STABLE completed its TGE in December 2025 and is used for staking and governance votes. Users see only a single asset, while operators and governance participants hold a separate coordination asset. It's a two-layer structure.

Note on governance-approved waivers and gasPrice 0: Stable lets governance-approved infrastructure providers ("waivers") submitgasPrice=0transactions to the network. The user signs an InnerTx withgasPrice=0, and the waiver wraps it in a WrapperTx broadcast to a designated marker address. From the user's perspective, the result is a fee-free transfer. To prevent abuse, waiver status is gated by a governance vote from STABLE holders. It's a design aimed at pushing payment UX as close to invisible as possible.

Canton sits at the most conservative end of the spectrum. Governance is run jointly by two entities: the Global Synchronizer Foundation (GSF), established in partnership with the Linux Foundation, and a separate Canton Foundation. The Super Validator set currently includes around 30 institutions, among them Digital Asset, Cumberland, Broadridge, Euroclear, SBI Digital Asset Holdings, Tradeweb, Talos, and Visa. Total node count is around 500. Transaction data is not broadcast to the whole network but distributed only to the parties to a given transaction. In a Delivery-versus-Payment (DvP) trade, for example, the bank transferring cash sees only the cash-side flow, and the share registry sees only the securities-side flow. The only parties that see both sides of the trade are the actual buyer and seller. This breaks the default assumption of public chains: that everyone sees every transaction.

Note on Canton Coin's burn-and-mint, and the parallel to Kaia CR: Canton Coin has no premine and no VC allocation. It's issued in proportion to network activity. In 10-minute rounds, Super Validators, ordinary validators, and Featured Apps receive activity coupons, which are then used to mint Canton Coin. Fees are denominated in USD, but settlement happens by burning Canton Coin. Any unminted portion of a round doesn't roll forward; it expires with that round.

This is philosophically close to the Contribution Reward (CR) Kaia is introducing in GP-21. Both systems share the principle that inflation only circulates in proportion to the value the network actually creates, and both remove the unachieved portion from circulation. The difference is scope. Canton Coin operates on a consortium-style institutional network by design, while Kaia CR applies to the inflation structure of a public mainnet itself. More on this later, but it's the most aggressive element of Kaia's tokenomics overhaul.

What these four chains share, and what they give up

Arc, Tempo, Stable, and Canton start from different places, but structurally they share the same set of choices. Mapped to the three axes of this article (Permissionless, Governance, Tokenomics), the pattern looks like this:

- Participation (Validator): All four chains deliberately curate validator participation today. Arc has an undisclosed set of 20 PoA operators. Tempo requires an onboarding process that involves "coordination with the team." Stable keeps its current operator list private. Canton runs an invite-only mainnet. From an institutional standpoint, the fastest way to establish clear accountability is to leave only "known operators" on the network.

- Governance: Authority lives in foundations, committees, and councils that sit outside the protocol. Canton's GSF / Canton Foundation / Super Validator structure is the most explicit example. Stable's STABLE-based governance, Arc's Circle-stewarded model, and Tempo's team coordination all converge on the same shape: institutional mechanisms outside the protocol hold the core authority.

- Tokenomics: The fee currency shifts to stablecoins (Tempo's USD, Arc's USDC, Stable's USDT0), or the payment layer is separated from the security layer entirely (Stable's STABLE versus USDT0). Either way, there's a clear shift away from economic models built on a volatile native asset.

One caveat is worth flagging. The claim that "you restrict validator participation to get predictability" doesn't hold up on its own. Features like sub-second deterministic finality or a stable gas currency can be achieved in a permissionless structure with many consensus participants. Kaia itself ran 1-second blocks and immediate finality even in its permissioned consortium phase, and intends to preserve that performance after the permissionless transition.

So why did these chains restrict validator participation to a known few, independently of performance goals? The answer lies less in engineering and more in practical accountability. When a payment fails, a compliance incident occurs, or the network has an outage, what institutions demand is "an operator that can meet an SLA" and "traceability of the policy decision path." This is a governance and accountability problem, not a technical one, and these chains chose the compromise of keeping the participant pool to a known few.

The bet, effectively, is that "selecting a responsible few" is faster than "building openness into the system itself." That isn't a wrong bet. It's just a different one from what Kaia proposes later in this article.

2.2 Public chains: open base, hidden curation

At the other end of the spectrum sit Ethereum and Solana. Both networks still hold to "anyone can be a validator" at the protocol level. Ethereum requires only 32 ETH and a validator client. Solana is technically open to anyone with enough SOL (the typical bar is tens of thousands, several million dollars as of April 2026) and the high-performance hardware to run a node.

But an open protocol doesn't mean an open operating economy.

Ethereum has the most open validator market at the protocol layer, yet the real operating economy is under strong centralization pressure. Liquid staking is the clearest axis of this concentration. Lido, the single largest protocol, has seen its share fall from roughly 30% to the low 20s as of April 2026. That is not a victory for decentralization so much as a reshuffling of where the concentration sits. Restaking-based liquid staking like EtherFi, plus centralized exchange (CEX) staking from Coinbase and Binance, have picked up the slack. The combined share of the top validator operators still accounts for more than half of all staked ETH. Institutional capital, for its part, flows toward staking-as-a-service providers with clearly defined legal entities. Lido's decline isn't being picked up by "more distributed participants." It's being picked up by other dominant players. Intermediation layers keep re-centralizing on top of an open base layer.

The same pattern repeats on the revenue side. As of April 2026, more than 90% of Ethereum blocks pass through MEV-Boost relays. A specialized layer of relayers and block builders (Flashbots, Titan, and others) has polarized validator economics. Enshrined PBS (ePBS), which pulls Proposer-Builder Separation into the protocol itself, is the main lever for reducing dependence on external MEV-Boost relays. It's likely to land in the Glamsterdam upgrade later in 2026, but isn't live at the time of writing. Even on the most open base layer, revenue distribution keeps concentrating in a specialized middle tier.

Solana focuses on trading openness for performance. The official recommended validator spec is 12+ core CPU, 256GB+ RAM, multiple enterprise NVMe drives, and a 1 Gbps link. But that's only the minimum floor. Top validators run well above it. As of early 2026, leading operators like Everstake, Helius, and Jito use 24-32 core CPUs, 512GB RAM, and 10 Gbps-class links as their production standard. And the top validators keep raising the bar. Running a competitive mainnet validator is no longer something a small participant can realistically afford.

The numbers make the concentration pressure even more visible. Validator count fell from around 2,560 in 2023 to roughly 770 by early 2026. The Alpenglow upgrade and the vote-fee restructuring could ease this, but neither has landed yet. On top of that, the Foundation's Delegation Program acts as a policy layer that distributes delegation based on performance and decentralization criteria, which means "who gets to operate" ends up decided by economics and policy together. Solana's "permissionless," then, is open at the protocol level but closer to a model where economics and operations do the curating in practice.

Ethereum and Solana go about it differently, but the lesson is the same. Keeping the base layer open is not, by itself, enough to preserve openness. The economic layer (staking concentration, polarized MEV revenue, break-even costs), the operating layer (hardware requirements, client diversity, foundation delegation programs), and the institutional layer each produce their own form of curation. When the protocol looks away, that curation happens anyway, just without explanation.

2.3 A third path for public chains: Avalanche institutional L1s

There's a third path, distinct from both Ethereum and Solana: the Avalanche L1 model. The Etna upgrade in December 2024 redefined the former Subnet model as L1s and reshaped the architecture significantly. The previous requirement for Subnet validators to lock 2,000 AVAX on the Primary Network was removed. Each L1 now maintains only its own state, rather than syncing the entire P-Chain, and pays only a dynamic monthly fee. This change lowered L1 deployment costs by roughly 99%.

The more structural change is the ValidatorManager contract (VMC). Each L1 manages its validator set directly via the VMC. The authority model can start as a multisig-based PoA, move to a stake-based permissionless PoS, or migrate to another model later through an upgradeable pattern. In effect, validator management itself has been separated at the contract level.

The institutional appeal shows up in the deployments. Franklin Templeton's BENJI, BlackRock's BUIDL, and Apollo's ACRED all picked Avalanche as a primary deployment target. Citi, Wellington Management, and WisdomTree ran private-markets tokenization proofs of concept on Spruce, Avalanche's institutional testnet. By February 2026, RWA volume on Avalanche had reached roughly $1.4B.

The trade-offs of this model are real. First, each L1 is responsible for its own security with its own validator set. An institutional L1 run by a small set of PoA validators ends up with security assumptions closer to a consortium chain. Second, the network effect of a single settlement layer weakens. Cross-L1 interoperability is technically possible, but liquidity and users fragment across L1s. Third, there's a disconnect in the value economy. With C-Chain fees drastically reduced and Primary Network staking lockups removed, the main sinks for AVAX shrank. VanEck notes that, as of early 2026, annual revenue fell about 42% year over year. The value that institutional L1s pay back to the Primary Network is only around $160k per year.

Avalanche's choice, summed up: stop trying to be a single settlement layer for institutions, and become a platform for custom institutional L1s instead. It's a third answer, different from the "one institution-friendly public chain" that Arc, Tempo, Stable, and Canton are aiming for, and different from the "open single L1" that Ethereum and Solana maintain. And different from Kaia's direction either.

2.4 Recap: the same problem, three different answers

Looking at all these chains through the three axes (Permissionless, Governance, Tokenomics), the industry's answers fall into roughly three camps.

- Institution-friendly single chains (Arc, Tempo, Stable, Canton) either curate all three axes directly, or absorb them into institutional mechanisms outside the protocol.

- Traditional public chains (Ethereum, Solana) leave all three axes open at the protocol level, while the actual curation happens in the economic and operating layers.

- The Avalanche L1 model lets each L1 decide for itself whether to stay open or curate, at the cost of giving up the network effect of a single settlement layer.

In our view, none of these three is a complete answer. The institution-friendly path weakens the neutrality case for public chains. Traditional public chains push accountability outside the protocol, leaving institutions to handle it themselves. The Avalanche L1 model gives up the network effect of being a single ecosystem. The real question isn't "permissioned or permissionless." It's what accountability structure permissionless gets layered on top of.

That's the question Kaia is asking.

3. Kaia's Answer: Accountable Permissionlessness

Kaia's original structure was a permissioned Governance Council (GC). Built on its Kakao and LINE legacy, the network was run by a consortium of validators. This worked well for securing early-stage and industry adoption. As Kaia blockchain started scaling out into onchain financial infrastructure, tying validator participation to the social hurdle of GC membership has become a growth bottleneck.

PGT (Permissionless, Governance, Tokenomics) is a structural redesign that addresses that bottleneck all at once. It isn't just a policy for growing the validator count. It's about putting openness, governance, and tokenomics back in alignment. The core can be summarized in three principles: Open participation. Separate roles. Measure performance through the system.

3.1 The permissionless transition: open, with performance guardrails intact

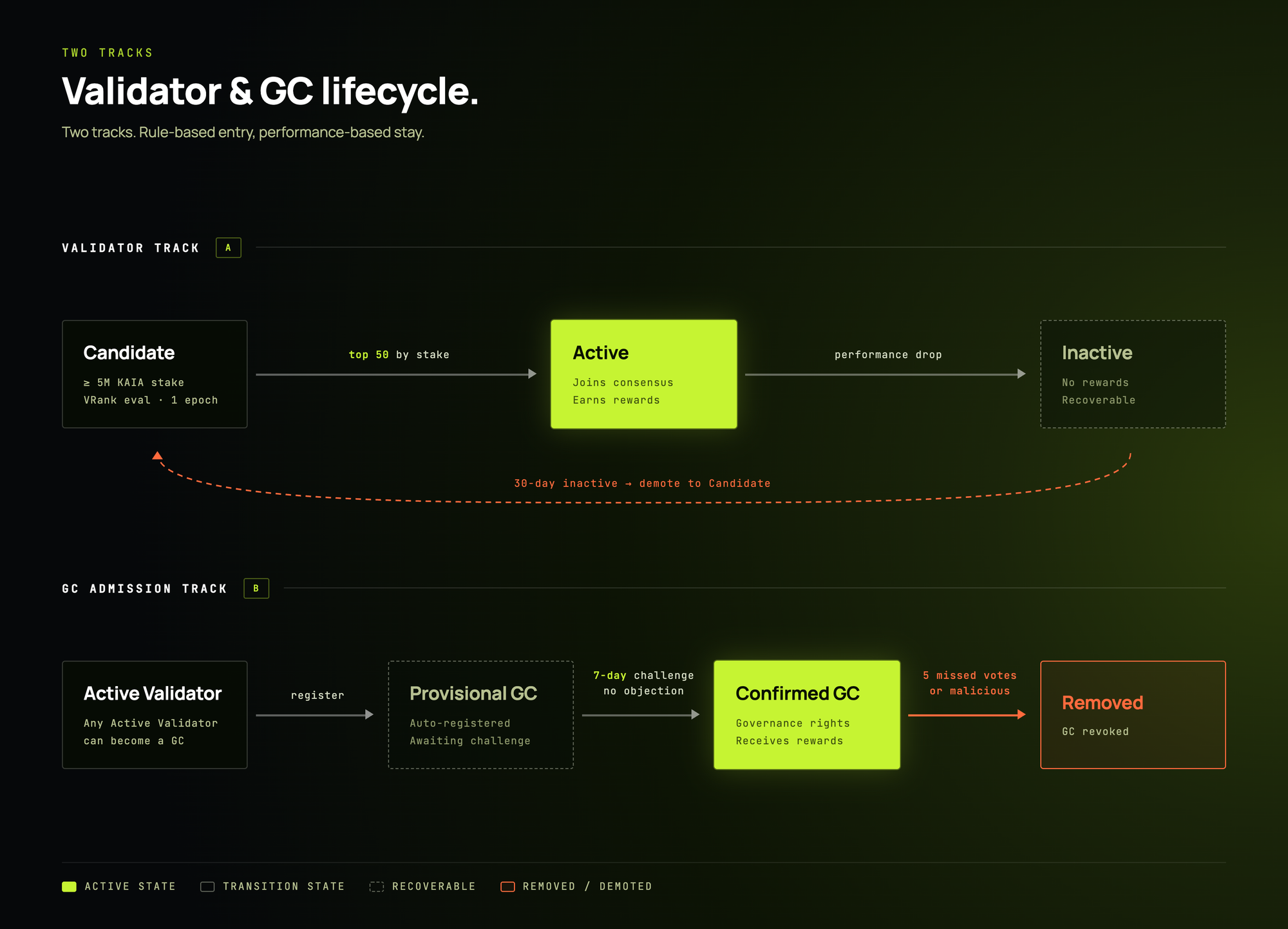

After the permissionless transition, anyone can become a validator candidate. But the entry bar is explicit. To become a Candidate, you must pass a VRank* evaluation over 1 epoch and meet a minimum stake of 5M KAIA. The Validator Pool is capped at 100, and only the top 50 by stake become Active Validators that participate in consensus. A validator that fails to meet performance criteria or keeps missing consensus rounds moves to an inactive state, and after roughly 30 consecutive days of inactivity is demoted back to Candidate. Rewards are paid only to Active validators.

Note on VRank: VRank is a performance-based evaluation metric that measures a validator candidate's operational capability onchain. It aggregates operating metrics like block production and validation success rates, network availability, response latency, and consensus-participation consistency on a per-epoch basis, and uses them to determine whether a Candidate is eligible to enter the active set. The point is to avoid granting eligibility based on stake amount alone. Instead of human approval, system-level metrics decide whether an operator can run the network. The detailed formula and weights will be finalized through public governance during implementation.

This design has an explicit trade-off. If opening consensus participation without any cap, performance and settlement finality start wobbling. Kaia's targets of 1-second blocks and immediate finality, plus the 10,000+ TPS goal after the 2026 KaiaBFT upgrade, are numbers that can only be sustained if the size of the consensus set is controlled. "Anyone can enter" becomes "anyone can enter and compete," and "anyone participates in consensus" becomes "top participants that meet system criteria participate in consensus."

An often-overlooked companion task here is Optimized Peer Discovery. Once the consensus set grows and validators start rotating in and out, the P2P design built for the old fixed-membership era can't handle the node-to-node topology anymore. Kaia is rolling out peer discovery optimization alongside the permissionless transition, so the network layer can handle a dynamic validator set.

Another practical change is easy to underestimate. The Permissionless Upgrade will remove proxy nodes and has GCs run only consensus nodes, which lowers node operating costs by roughly 50%. This isn't just an optimization. Many networks' permissionless approach leave the operating-cost structure untouched. But for new validators to actually show up, both the capital requirement and the OPEX structure have to come down. Kaia is one of the few public chains that addresses openness and operating costs together.

3.2 GC redesign: automatic entry, explicit accountability

Another core change with the Permissionless Upgrade is separating the validator role from the GC role. In the old structure, the GC and the validator were effectively the same entity, and a new participant's entry required approval from existing GC members. This was justified in the early phase, but as the network grew, it produced two problems. First, existing members' interests could disproportionately shape new admissions. Second, without a clear split between operating responsibility and policy authority, tracing accountability became difficult.

After the permissionless transition, the GC admission path fundamentally changes. Once a participant with validator eligibility completes GC attestation, public proposal, and required information registration, they're automatically registered as a Provisional GC. If no structural objection is raised during a default 7-day challenge window, they're automatically confirmed as a Confirmed GC. The default flips to "pass without existing-member approval." The objection mechanism stays, but the gate where approval had to be actively given is gone.

Meanwhile, the accountability mechanisms tighten. Because the GC is a role layered on top of validator responsibility, losing validator eligibility automatically forfeits GC eligibility. If a GC misses 5 consecutive governance votes, a removal motion can be put on the agenda. Malicious behavior or attestation errors are also grounds for losing status. Entry is automated, but the conditions for staying in are explicit and enforced.

This doesn't mean "validator equals governance." Kaia ports into public chains a structure traditional finance has long used: the separation of operating committee and policy committee. Validators run operations, the GC runs policy. They are separate, but connected by a chain of responsibility. That's why the design is more complex than simple stake-weighted governance, and it's also why, from an institutional perspective, the role structure looks more familiar.

This is why Kaia's permissionless isn't a laissez-faire model, and rather the accountable permissionlessness. Eligibility is decided by the system, authority is split by role, and performance is measured onchain.

4. Revisiting MEV: Where Does Fairness Come From?

The topic most often missing from permissionless discussions is MEV. But in practice, the moment you make a chain permissionless, MEV is the first thing that gets distorted.

Ethereum's experience is instructive. At the protocol level, the validator market is open. But with more than 90% of blocks today passing through MEV-Boost relays, specialized relayers and block builders have accumulated a revenue advantage that polarizes validator economics. As a result, "anyone can become a validator" still holds, but "all validators have a similar revenue structure" has broken down. This is why ePBS is getting serious attention in the Glamsterdam upgrade slated for 2026. The goal is not to eliminate MEV but to pull it into the protocol so it no longer centralizes the validator verification layer.

Kaia has already started building toward this with KIP-249 MEV Auction in 2025. The rights to produce a block are auctioned, and the auction proceeds are redistributed both as validator rewards and at the protocol level. This design aims at three effects.

First, MEV moves from a hidden private trade to an observable public market. Who paid what, and which transactions received priority, is recorded onchain as an auction outcome.

Second, MEV revenue is folded into validator rewards rather than captured by a specialized group. This keeps opening up the validator set from turning into a "market where entering yields no return." If you declare permissionless while revenue keeps concentrating among a few specialists, the opening is effectively a step backward.

Third, the roadmap points toward an Open MEV Auction. What exists today is a protocol-level auction based on KIP-249. During 2026, it will combine with a more open builder marketplace, moving the entire MEV economy toward transparent public infrastructure.

Kaia's position: MEV isn't something to eliminate. It's a question of how to distribute value that inevitably shows up on a high-performance chain. Fairness comes not from the absence of MEV, but from its observability and from how it's redistributed.

This lines up with how institutions already see the world. For them, MEV's existence isn't a surprise. Traditional financial markets have always had an economy around order flow and priority placement. The question is whether that economy is observable, has clear rules, and is designed for fair participation. Kaia's MEV Auction is an attempt to meet those conditions at the protocol level.

5. Redesigning Tokenomics: Inflation Should Be a Performance-Based Contract

Where Kaia most sharply diverges from other chains isn't validator openness. It's tokenomics.

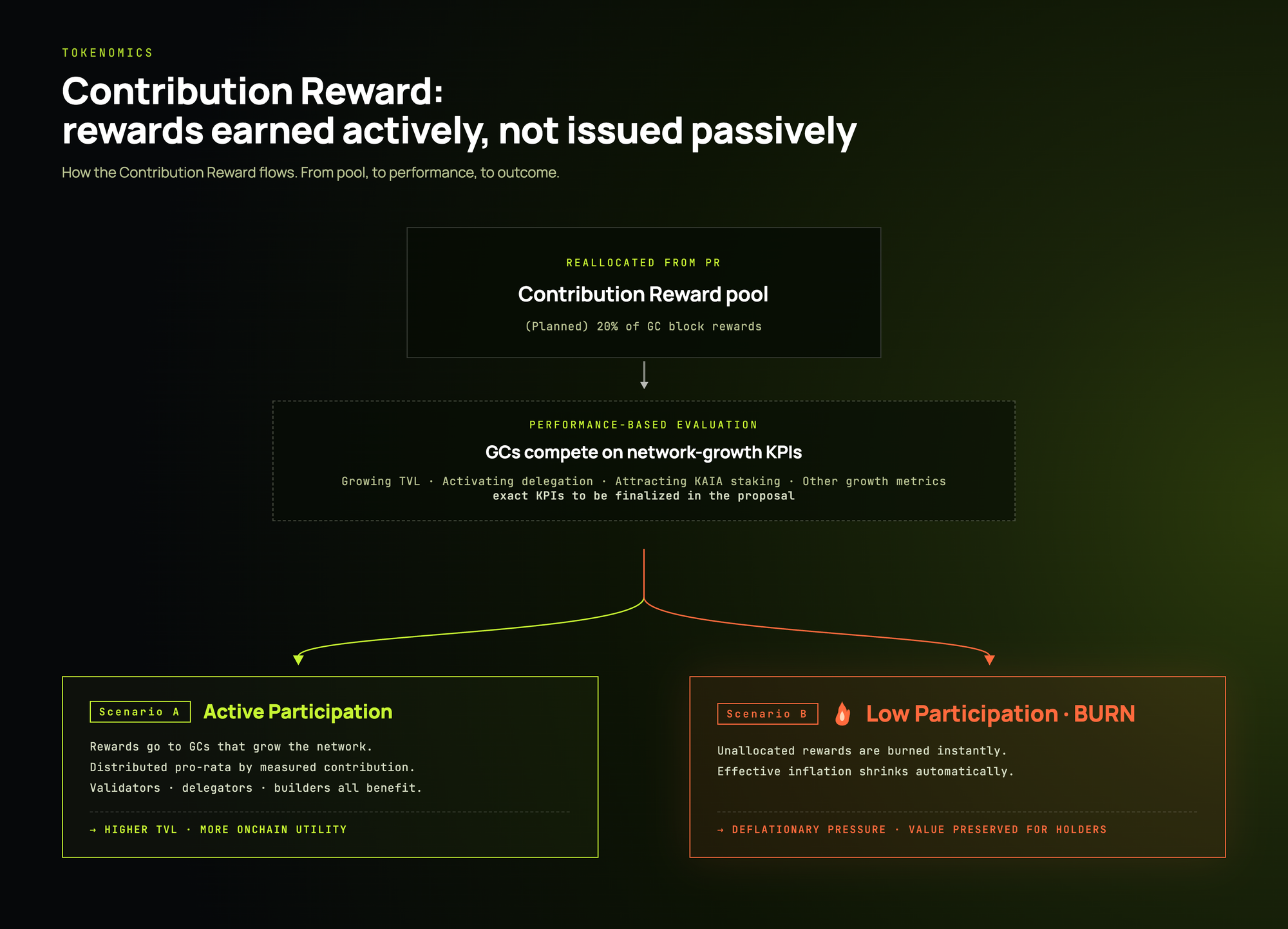

Under the current structure, Kaia's annual inflation is roughly 4.87%. Block issuance is 9.6 KAIA, 50% of which is allocated to the GC and community. That share is further split between Staking Reward (SR) and Proposer Reward (PR). We wanted to restructure the PR. PR is allocated equally to every GC that participates in block generation, regardless of whether they contributed to network growth, attracted user delegation, or grew stablecoin TVL.

As a subsidy for early-stage stability, this structure is understandable. But it becomes hard to justify in a network aiming to be onchain financial infrastructure. In an environment where institutional capital flows in and stablecoins, RWAs, and payment rails are being built on top, validators have to be more than block-production machines. Driving ecosystem growth is the responsibility of new GCs/Validators. Equal-share PR doesn't map to that broader role.

5.1 From PR to CR: redesigning the distribution layer

The core of GP-21 aims at replace PR with CR, and SR stays. The existing PR allocation, however, is distributed in proportion to measurable onchain contribution. The initial metrics are TVL contribution to Kaia Foundation-designated protocols, user delegation activation, and KAIA staking participation.

The most important design point here is the immediate burn of unachieved rewards. Rewards allocated but not earned don't roll forward. They're burned immediately. Under the same nominal inflation, the effective circulating supply flexes with actual contribution. When activity is high, more rewards go to meaningful contributors. When activity is low, undistributed rewards are burned and effective inflation shrinks automatically.

The implication goes far beyond a simple change in reward ratios. Kaia redefines inflation not as "an operating subsidy" but as "a contract that only pays out when there's performance." Philosophically this is similar to Canton's burn-and-mint, discussed earlier, but Canton's design operates on a consortium-style institutional network. Kaia's CR applies the same philosophy directly to the inflation structure of a public main chain. That's a much more aggressive choice.

5.2 What the initial parameters tell us

CR's initial operating parameters aren't just abstract. CR participation requires KAIA staking or delegation. The USDT deposit cap is calculated at a 10 KAIA to 1 USDT ratio, proportional to stake. A GC can set a commission of at least 20% on the CR boost that a user receives. The initial TVL KPI is 50M USDT, and the designated protocols are SuperEarn and Unifi.

These numbers tell us two things. First, CR isn't a simple yield-farming play. Staked KAIA and onchain USDT TVL are linked in a ratio, so CR only activates when KAIA governance capital and stablecoin liquidity grow together. Second, they name a threshold: the 50M USDT KPI is what Kaia describes as "the structural threshold at which liquidity starts self-circulating." Below that band, CR APR tends to balloon and attract only mercenary liquidity. Kaia names the threshold directly and designs conservatively around it.

The design carries tensions too. Choosing designated protocols, qualitatively evaluating KPIs, and judging whether TVL is "good capital" or "capital responding to subsidies" are not easy problems. In the same vein, the GP-21 document presents three options for the SR/CR ratio (Option A 80/20, Option B 70/30, Option C 60/40) and leaves them open for governance discussion. How aggressive performance-based incentives should be is still an open parameter.

The direction, though, is clear. What public chains need right now isn't just to cut inflation. It's a structure in which inflation functions as a healthy incentive. That's where Kaia is heading.

5.3 The downside of performance-based rewards

One risk is worth naming directly. Performance-based rewards redefine validators from simple "infrastructure operators" into more complex "ecosystem growth partners." That's the intended direction. But if the metrics are poorly designed, the structure can end up rewarding the best partnership dealers more than the best validators.

Kaia is aware of the risk. Foundation-designated protocol selection, KPI design, and CR commission caps are the levers Kaia uses to control early-stage distortion. The structure is also built as a tunable governance experiment, not as a set of fixed parameters, so it can keep being refined over time.

6. Why Now, and Where Next

6.1 Why now

Why PGT matters for Kaia right now is simple. This isn't an abstract overhaul for demand that hasn't arrived yet.

Kaia has already completed the native deployment of USDT and secured deposit/withdrawal support at major exchanges. It has also onboarded regional fiat-linked stablecoins such as KRW Stablecoin (upcoming), JPYC (upcoming), IDRX / IDRP, and MYRC. Through fee delegation and gas abstraction, users can interact with the network without having to hold KAIA first. Beyond that, RWA projects like OpenEden's yield-bearing stablecoin and Goldstation's gold-linked token are already running on Kaia.

The most telling move is Yield8. It's an onchain fund from Kaia Investment Partners (KIP) targeting 8%+ APR in Asian private credit. The underlying assets come from three strands: Galactica, which covers Indonesian shipping finance; YieldCore, which wraps Korean gas station inventory in a BNPL format; and Forest Jalan, which focuses on loans to small-business owners and workers in Indonesia. Distribution runs through SuperEarn, a protocol incubated by the Kaia ecosystem. Yield8 alone shows a model where chain, product, and the distribution layer all move together under a single ecosystem strategy. Rather than passively waiting for institutions to arrive, Kaia is actively co-building institutional-grade products on the chain.

PGT, then, is the initiative of realigning validators, governance, and tokenomics for the next step on top of a network where the stablecoin financial stack is already forming. Rather than laying down infrastructure first and waiting for demand, the protocol is being reshaped around demand that's already in motion.

6.2 The competitive landscape

External market conditions are moving in the same direction. As noted earlier, Arc is publicly considering a transition from PoA to permissioned PoS and introducing a native token. Tempo is preparing for a post-mainnet permissionless transition while pulling in payment and custody players like Visa, Stripe, and Zodia as anchor validators. Canton already operates Super Validator governance with 31 institutions. Stable runs a two-layer structure that keeps only USDT visible to users, with governance handled separately under STABLE. Avalanche L1 positions itself as a platform for custom institutional chains and has drawn in large RWA deployments like BlackRock BUIDL, Franklin Templeton BENJI, and Apollo ACRED.

The shared conclusion across all these designs: any chain aiming at onchain finance eventually has to redesign its validator structure, governance structure, fee unit, and privacy model together. Partial improvements don't cut it structurally.

Kaia's take on that shared conclusion is a little different. Being an institutional-grade blockchain doesn't require narrowing the validator set again. What it does require is systematizing openness more rigorously: who can participate in operations, who can perform governance, and who can receive rewards should be decided on public eligibility and onchain performance, not on human reputation or internal consensus. That’s what the Permissionless upgrade would deliver on Kaia, and that’s what accountable permissionlessness means.

6.3 What's next: Agentic Validator / GC Management

This direction continues beyond 2026. The "Later" section of the roadmap introduces Agentic Validator / GC Management, a phase where repetitive judgments like validator eligibility evaluation, performance monitoring, GC challenge triggering, and CR KPI adjudication get partially automated by AI agents.

This isn't just UX. For permissionless to function at scale, eligibility evaluation and accountability tracing grow beyond what manual human processes can handle. Dynamically managing a 100-validator pool, tracking delegation flows, and adjudicating dozens of designated-protocol KPIs at once does not scale under purely human-operated governance. Flagging an agentic management layer as the next phase after the permissionless transition signals one recognition: as the scale of openness grows, the judgment infrastructure has to evolve along with it.

Wrapping up

The core message of Permissionless Kaia isn't "let's be more decentralized." It's more specific than that: Public financial infrastructure should be permissionless, but permissionless can't become another word for irresponsibility.

Validators need to bear operational responsibility contributing to the participating blockchain network. Governance needs to be separated from operations, and the separation needs to be explicit. Inflation needs to be justified by contribution. MEV should be surfaced into a public market rather than hidden. And the operating-cost structure has to be redesigned alongside the openness discussion. Only when all these conditions move together can a public chain truly serve as the foundation for institutional-grade onchain finance.

PGT is the design for that transition. And this isn't Kaia's problem alone. It's a question the entire public-chain space has to face as it moves into the next stage of onchain finance. We think the answer is still open. Kaia is trying to find it by opening up more precisely, not by narrowing down participation.

The next piece in this series looks at what user layer actually lands on top of this opened base. It's about an era where AI agents, not humans, show up onchain as real users, and about the world of Agentic Commerce and Agentic Payment, where value gets exchanged autonomously on top of that base. We'll look at what Kaia is building with Trustless Agents (ERC-8004), Agent-to-Agent(A2A) Payment, and the DeFAI Agent Marketplace. When the users on top of a permissionless base change, the questions the infrastructure has to answer change with them.