Architectural Insight Report: Rewiring Cross-Border Remittance with Institutional Stablecoins on Kaia

Our latest Stablecoin PoC Insight Report proves the viability of blockchain for cross-border remittances. By proving a more efficient alternative to legacy systems like SWIFT, our KRW stablecoin pilot achieved sub-3-second transactions and reduced cross-border costs by 87%.

Focus: Phase 0 Proof of Concept (PoC) – KRW Stablecoin Issuance, Payment, and Cross-Border Remittance

Partners: K-STAR Alliance (OpenAsset, AhnLab ABC, Lambda256)

Executive Summary

Real-world adoption of blockchain technology by Tier-1 financial institutions requires moving beyond theoretical use cases and testing actual, battle-hardened infrastructure. In Q1 2026, the Kaia blockchain network served as the foundational settlement layer for a landmark "Phase 0" Proof of Concept (PoC) led by a Tier-1 Korean bank and the K-STAR Alliance; a consortium of domestic leaders in stablecoin infrastructure.

The objective of this PoC was to functionally validate the end-to-end lifecycle of a fully backed Korean Won stablecoin across four core pillars: Issuance, Charging, Retail Payment, and Cross-Border Remittance.By settling transactions entirely onchain as an alternative to correspondent banking networks (SWIFT), the PoC achieved sub-3-second settlement times and reduced cross-border transaction costs by nearly 87%. Furthermore, the PoC successfully integrated with leading Korea-based payment gateways for offline retail payments, proving that Web3 infrastructure can seamlessly interface with legacy Web2 point-of-sale systems.

This report details the technical architecture of the PoC, the performance metrics achieved, the remaining compliance hurdles, and the strategic roadmap for commercialization and Real World Asset (RWA) integration on Kaia.

1. Market Context: The $900 Billion Asian Stablecoin Opportunity

The global financial system is currently undergoing a paradigm shift. Jurisdictions are increasingly moving to protect their monetary sovereignty by encouraging the issuance of local-currency stablecoins to counterbalance the dominance of USD-pegged assets.

According to market projections, the global stablecoin market is expected to grow 15x to $3 Trillion within the next five years. Applying regional M2 money supply ratios, the Serviceable Available Market (SAM) for Asian stablecoins is projected to reach $900 Billion, with the South Korean market alone accounting for a $150 Billion opportunity.

Currently, cross-border remittances and B2B settlements in Asia rely on a fragmented network of correspondent banks communicating via SWIFT's ISO 20022 (SWIFT_MX) messaging. This legacy architecture is capital inefficient (requiring pre-funded Nostro/Vostro accounts), slow (1-3 business days), and expensive. This PoC was designed to test whether Kaia’s public ledger could replace this messaging and settlement layer with a single, unified state machine.

2. Phase 0 Architecture: Bridging TradFi and Web3

To simulate a real-world institutional environment, the PoC utilized a controlled testing environment on the Kaia network, integrating deeply with OpenAsset’s enterprise-grade tokenization infrastructure. The architecture relied on two primary OpenAsset products:

- OPEN(MINT): A Stablecoin-as-a-Service (SaaS) platform that handles the secure issuance of KRW-backed stablecoin.

- WHITELIST: A digital asset custody wallet focused on internal control and asset protection. It enforces strict access controls, ensuring that KRW-backed stablecoins can only be transferred to pre-verified, KYC/AML-compliant addresses, thereby mitigating the risk of interacting with tainted anonymous liquidity.

3. The End-to-End Transaction Lifecycle

The PoC successfully executed and validated four distinct operational flows on the Kaia blockchain:

A. Issuance and Charging

The process began with simulating a banking environment. A user requested a deposit of traditional KRW from their bank account into the digital asset service. Upon receipt of the fiat, an equivalent amount of onchain KRW was minted on the Kaia network. The newly minted KRW was then credited to the user's wallet.

B. Offline Retail Payment

To prove everyday utility, the PoC tested an offline retail payment at a well-known coffee chain.

- The Flow: The user scanned a QR code at the kiosk using their bank’s wallet.

- The Settlement: The transaction was routed through a major Korean Payment Gateway provider. The Kaia network processed the transfer of onchain KRW from the user's wallet to the merchant's wallet instantly.

- The Off-Ramp: The merchant portal allowed for immediate settlement, converting the received onchain KRW back into traditional KRW for deposit into the merchant's corporate bank account.

C. Cross-Border Remittance (Bypassing SWIFT)

The most technically complex and impactful phase of the PoC was the cross-border remittance to Vietnam (VND).

- The Swap: The user initiated a transfer of onchain KRW. Using an onchain liquidity pool, the KRW stablecoin was swapped for USDT (acting as the intermediate global routing asset).

- The Off-Ramp: The USDT was routed to a local off-ramp partner in Vietnam.

- The Payout: The off-ramp partner received the onchain USDT, converted it to local fiat, and disbursed VND directly to the recipient's bank account.

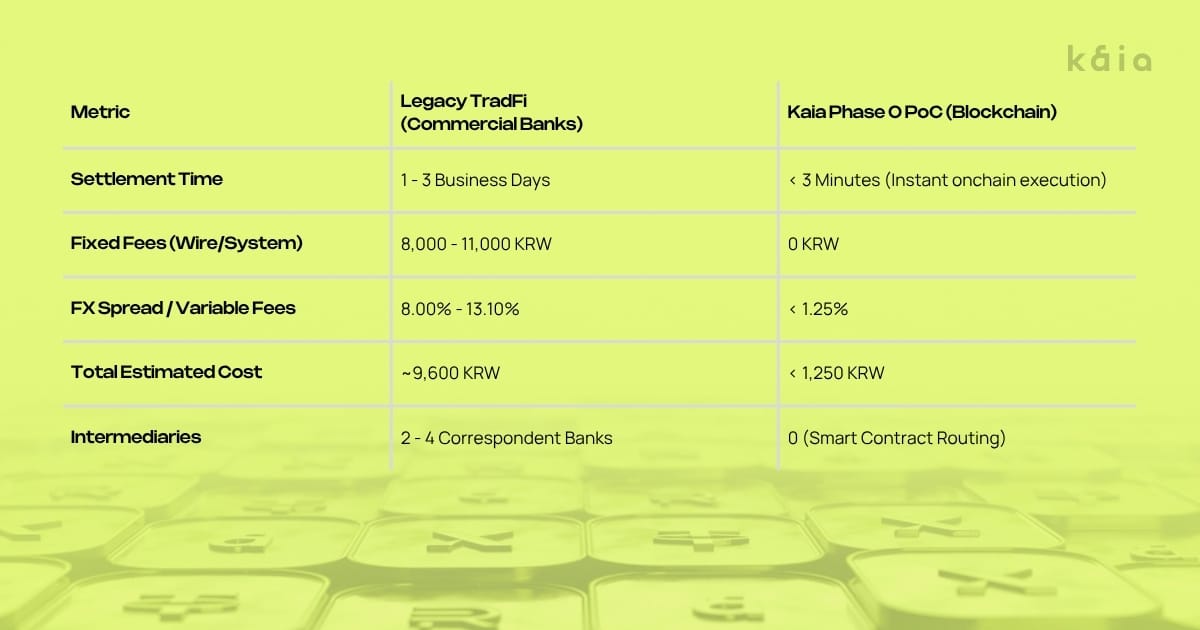

4. Performance Metrics vs. Legacy Systems

The data extracted from the Phase 0 test highlights the massive efficiency gains provided by Kaia's blockchain infrastructure. Based on a simulated transfer of 100,000 KRW to Vietnam, the cost breakdown was as follows:

5. Unresolved Challenges & Engineering Hurdles

While the PoC executed flawlessly from a functional standpoint, transitioning from a Phase 0 test to a production-ready enterprise solution requires addressing several critical technical and regulatory challenges:

- Onchain Settlement Stress Testing: While the PoC validated the logic, future phases must conduct rigorous TPS (Transactions Per Second) stress testing to ensure the Kaia network can handle the volume of a national commercial bank's daily retail clearing.

- Compliance & The Travel Rule: Public blockchains natively transfer tokens, but they do not natively transfer the required KYC/AML data payloads. Future development requires implementing ISO 20022 messaging standards alongside smart contract executions to ensure full regulatory compliance.

- Direct FX Liquidity Pools: Relying on USDT as an intermediate routing asset introduces secondary market volatility. The goal is to establish direct, private liquidity pools (e.g., KRW stablecoin directly to local Asian stablecoins) to further compress slippage and fees.

6. Strategic Roadmap and Future Synergies with Kaia

The successful completion of Phase 0 paves the way for a multi-year roadmap aimed at commercialization and ecosystem expansion. In partnership with leading banking institutions, Kaia and the K-STAR Alliance are exploring several new business opportunities:

Phase 1 to 3: Commercialization & Ecosystem Expansion

- Phase 1 (Commercial Pre-Development): Focuses on deep banking integration, global stablecoin payment environments, and building a regulatory-compliant remittance pipeline (especially for strict jurisdictions like the US).

- Phase 2 (Ecosystem Creation): Explores integrating onchain KRW with the Bank of Korea's CBDC initiatives (using CBDCs as 1:1 collateral for stablecoin issuance) and implementing Purpose Bound Money (PBM) for transparent local government subsidies and grants.

- Phase 3 (Market Leadership): Full consortium formation, comprehensive digital asset payment routing, and global On/Off ramp dominance.

New Business Proposal: One-Click Stablecoin Yield & RWA Integration

Beyond payments, the most lucrative use case for stablecoins is yield generation backed by Real World Assets (RWAs). Kaia and its partners are exploring infrastructure that allows users to deposit KRW stablecoins via their banking apps to access stable, low-risk yields.This involves expanding beyond simple treasury bills into high-yield, real-economy asset classes. Proposed integrations on Kaia include:

- Galactica: Ship bridge loans and second-hand vessel financing with Korindo (a top 10 Indonesian conglomerate).

- Forest Jalan: Micro-lending RWAs for small business owners, powered by partnerships with regional super-apps like Grab.

- Yield Core: Gas station accounts receivable-backed loans with built-in oil price hedging, structured alongside major domestic securities firms.

7. Conclusion

The Phase 0 PoC successfully proved that the core premise of blockchain-based finance (bypassing intermediary institutions for instant, low-cost settlement) is functionally viable for Tier-1 institutions. By integrating OpenAsset's secure issuance infrastructure with the high-performance Kaia network, the Korean banking industry has taken a definitive step toward the future of digital banking.

Moving money onchain is technologically simple; moving money onchain in a way that satisfies global regulatory frameworks, integrates with legacy POS systems, and protects institutional capital is the actual challenge.

This PoC proved it can be done. As we solve the remaining compliance and liquidity routing challenges, Kaia is uniquely positioned to serve as the primary settlement layer for the next generation of Asian Web3 finance.

Also read: Hard Assets, Digital Rails: The RWA Thesis for the Kaia Ecosystem